Top story News and analysis

Young people opting

out of auto-enrolment

Data has shown that the number of employees under 40 opting out has

increased, possibly because of other financial pressures. By EMMA GREEDY

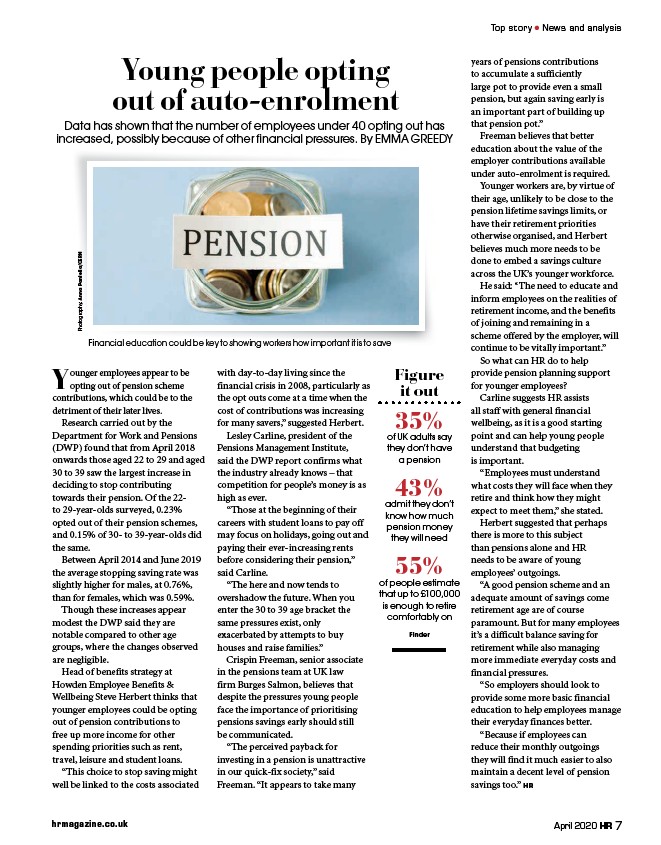

Financial education could be key to showing workers h how important it is to save

Figure

it out

35%

of UK adults say

they don’t have

a pension

43%

admit they don’t

know how much

pension money

they will need

55%

of people estimate

that up to £100,000

is enough to retire

comfortably on

Finder

Photography: Anna Pantelia/CERN

Younger employees appear to be

opting out of pension scheme

contributions, which could be to the

detriment of their later lives.

Research carried out by the

Department for Work and Pensions

(DWP) found that from April 2018

onwards those aged 22 to 29 and aged

30 to 39 saw the largest increase in

deciding to stop contributing

towards their pension. Of the 22-

to 29-year-olds surveyed, 0.23%

opted out of their pension schemes,

and 0.15% of 30- to 39-year-olds did

the same.

Between April 2014 and June 2019

the average stopping saving rate was

slightly higher for males, at 0.76%,

than for females, which was 0.59%.

Though these increases appear

modest the DWP said they are

notable compared to other age

groups, where the changes observed

are negligible.

Head of benefits strategy at

Howden Employee Benefits &

Wellbeing Steve Herbert thinks that

younger employees could be opting

out of pension contributions to

free up more income for other

spending priorities such as rent,

travel, leisure and student loans.

“This choice to stop saving might

well be linked to the costs associated

with day-to-day living since the

financial crisis in 2008, particularly as

the opt outs come at a time when the

cost of contributions was increasing

for many savers,” suggested Herbert.

Lesley Carline, president of the

Pensions Management Institute,

said the DWP report confirms what

the industry already knows – that

competition for people’s money is as

high as ever.

“Those at the beginning of their

careers with student loans to pay off

may focus on holidays, going out and

paying their ever-increasing rents

before considering their pension,”

said Carline.

“The here and now tends to

overshadow the future. When you

enter the 30 to 39 age bracket the

same pressures exist, only

exacerbated by attempts to buy

houses and raise families.”

Crispin Freeman, senior associate

in the pensions team at UK law

firm Burges Salmon, believes that

despite the pressures young people

face the importance of prioritising

pensions savings early should still

be communicated.

“The perceived payback for

investing in a pension is unattractive

in our quick-fix society,” said

Freeman. “It appears to take many

years of pensions contributions

to accumulate a sufficiently

large pot to provide even a small

pension, but again saving early is

an important part of building up

that pension pot.”

Freeman believes that better

education about the value of the

employer contributions available

under auto-enrolment is required.

Younger workers are, by virtue of

their age, unlikely to be close to the

pension lifetime savings limits, or

have their retirement priorities

otherwise organised, and Herbert

believes much more needs to be

done to embed a savings culture

across the UK’s younger workforce.

He said: “The need to educate and

inform employees on the realities of

retirement income, and the benefits

of joining and remaining in a

scheme offered by the employer, will

continue to be vitally important.”

So what can HR do to help

provide pension planning support

for younger employees?

Carline suggests HR assists

all staff with general financial

wellbeing, as it is a good starting

point and can help young people

understand that budgeting

is important.

“Employees must understand

what costs they will face when they

retire and think how they might

expect to meet them,” she stated.

Herbert suggested that perhaps

there is more to this subject

than pensions alone and HR

needs to be aware of young

employees’ outgoings.

“A good pension scheme and an

adequate amount of savings come

retirement age are of course

paramount. But for many employees

it’s a difficult balance saving for

retirement while also managing

more immediate everyday costs and

financial pressures.

“So employers should look to

provide some more basic financial

education to help employees manage

their everyday finances better.

“Because if employees can

reduce their monthly outgoings

they will find it much easier to also

maintain a decent level of pension

savings too.” HR

hrmagazine.co.uk April 2020 HR 7

/hrmagazine.co.uk